Inflation, housing costs, climbing insurance premiums, and heavier debt loads. South Carolina families are getting squeezed from every direction at once. For most households, the word “bankruptcy” only enters the conversation after months of trying to keep up, and by then the pressure can feel suffocating.

Available data appears to support that observation. Bankruptcy filings rose 12% across South Carolina in the year ending December 31, 2023, pointing to a growing need for formal financial relief. During that same stretch, Chapter 13 filings jumped 14%, a sign that more residents are seeking structured ways to reorganize what they owe rather than just walk away from it.

Housing-related financial pressures may be contributing to these challenges. Foreclosure rates in the state have stayed among the highest in the country in recent years, and one report noted that South Carolina ranked second nationally for foreclosures in April 2026, with one in every 1,745 housing units facing a filing. When you’re staring down that kind of financial distress, getting reliable information early (before panic takes over) can help you make strategic decisions instead of reactive ones.

People are also reading…

Why More South Carolinians Are Considering Bankruptcy

Debt pressure is hitting on multiple fronts

It’s not just one bill that’s become unmanageable; it’s several at the same time. The average South Carolinian owed roughly $56,600 in household debt in 2024, with mortgage loans accounting for 65.3% of that total. Balances that high leave almost no cushion for a surprise medical bill, a sudden layoff, or even an expensive car repair. Many individuals and families face similar circumstances.

In fact, 37% of South Carolinians currently have debt in collections, which tells you just how widespread these budgeting shortfalls have become.

Foreclosure data shows why timing matters

The risk of losing a family home has increased in some parts of the state, prompting homeowners to seek information about their legal options. In March 2024, South Carolina recorded one of the highest foreclosure rates in the country, a stark reminder of how fast financial strain can spiral into a full-blown housing emergency. Homeowners who bought near the top of the market are now getting squeezed by elevated mortgage rates, skyrocketing insurance premiums, and rising ownership costs that didn’t exist when they signed the papers.

This local surge mirrors what’s happening nationally. Foreclosure rates hit six-year highs in the first half of 2024 across the United States. For South Carolina families, one key consideration is: acting early, even a few weeks sooner, can make a real difference when you’re trying to protect your home.

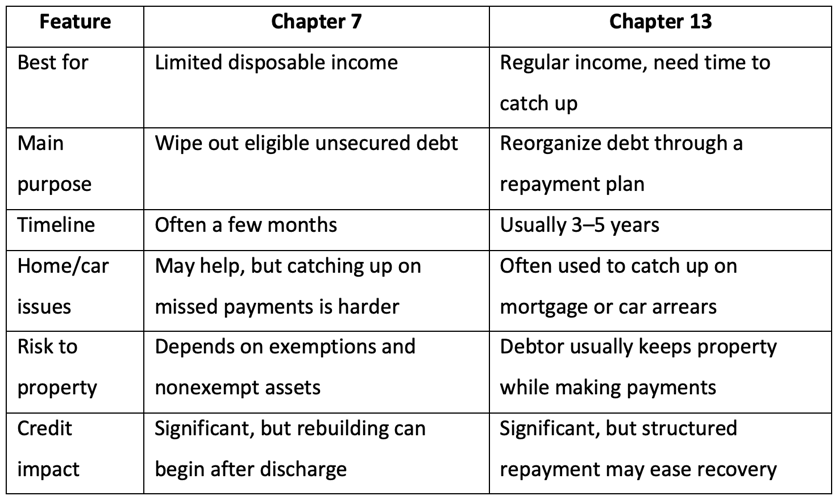

Chapter 7 vs. Chapter 13: The Difference That Matters Most

When Chapter 7 may make sense

If you’re drowning in credit card balances and medical bills with little disposable income to show for it, Chapter 7 is probably the route you’ll hear about first. It’s designed for people who simply can’t realistically pay back their creditors over time. The focus is on discharging eligible unsecured debt (think high-balance credit cards and unexpected medical bills), which tend to make up the bulk of consumer financial distress.

There’s a catch, though. A court-appointed trustee can sell nonexempt assets to repay creditors, although South Carolina exemption laws do protect certain types of property, including basic household goods and affordable vehicles. The process itself typically wraps up in just a few months, which is one reason many filers choose this path to quickly halt collection activity. If speed and a clean break are your priorities, Chapter 7 is often where the conversation starts.

When Chapter 13 may be the better fit

Now, if you’re earning a steady paycheck but just need breathing room to catch up on what you’ve fallen behind on, Chapter 13 works differently. It’s built specifically for people with regular income who prefer to reorganize their debts rather than liquidate assets. The court approves a repayment plan lasting three to five years, rolling past-due balances into a single, manageable monthly payment.

Homeowners gravitate toward this option when they’re behind on their mortgage or auto loan but desperately want to keep the house or the car. Think of it like hitting a structured pause button: You stay in the property while catching up under court supervision. The jump in Chapter 13 filings in South Carolina in late 2023 suggests this tool is becoming more popular for exactly that reason.

Quick side-by-side comparison

Here’s a snapshot of how the two chapters stack up against each other:

Can Bankruptcy Stop Eviction or Foreclosure?

How the automatic stay works

An immediate benefit of bankruptcy filing is something called the automatic stay, which kicks in the moment your petition hits the court clerk’s desk. This legal provision generally pauses most collection actions: collection calls, wage garnishments, and pending lawsuits. Creditors are prohibited from taking further steps to collect what you owe without specific permission from the judge.

For South Carolinians facing the imminent loss of property, the stay may temporarily halt foreclosure sales and certain types of eviction activity, buying you crucial time to assess your options. Federal courts enforce this stay to give debtors a window to organize their finances without the constant threat of immediate asset seizure. It’s not a permanent shield, but it can be a lifeline when you need breathing room.

Foreclosure: why Chapter 13 is often part of the conversation

When your family home is scheduled for a public auction, choosing the right chapter becomes critical. Chapter 13 can give homeowners time to make up for missed mortgage payments through a court-approved repayment plan while they remain in the house. Chapter 7, by contrast, may temporarily delay a foreclosure through the automatic stay, but it typically doesn’t provide a long-term mechanism to cure mortgage arrears.

Here’s the reality: Since the lender can eventually petition the court to lift the stay, relying on a liquidation chapter alone rarely saves a heavily delinquent property for good. Homeowners who wait too long to explore their legal options risk losing their homes entirely.

Eviction cases are more complicated

If you’re a renter dealing with the threat of losing your housing, the rules get murkier. While the federal stay may pause some preliminary eviction actions, how much protection you actually get depends heavily on the timing of your landlord’s lawsuit. If a landlord has already obtained a final judgment for possession from a local magistrate before you file, federal protection may be limited or unavailable. Not the answer you were hoping for, right?

That’s why anyone facing an immediate housing deadline should carefully assess their specific situation to avoid an unexpected lockout. If you need more details on stopping foreclosure, navigating eviction, or avoiding common filing mistakes, you can review these South Carolina bankruptcy resources. Also, understanding lease default rules under the bankruptcy code can help prevent sudden displacement, especially if you’re unsure where you stand.

What You Need to Do Before Filing

The Basic Steps to Take Before You File

Filing a bankruptcy petition requires organization, transparency, and a clear picture of your complete financial situation. Without thorough preparation, you risk having your case dismissed or losing assets that could’ve been protected under South Carolina law. The court demands accuracy under penalty of perjury. Gathering the necessary paperwork early may help streamline the process and reduce the likelihood of administrative delays.

Before your paperwork can even be accepted by the clerk, you’ll need approved credit counseling through a Department of Justice provider. Following a clear sequence of steps helps your petition move through the federal system without unnecessary delays or creditor objections. Here’s the checklist:

- Complete a credit counseling course from an approved provider.

- Gather pay stubs, tax returns, bank statements, and monthly bills.

- Make a full list of debts, creditors, assets, and regular expenses.

- Review whether you’re facing eviction, foreclosure, repossession, or wage garnishment.

- Decide if Chapter 7 or Chapter 13 is a better fit for your income and goals.

- Get legal advice if you own property, have recent asset transfers, or owe priority debts like taxes or child support.

Documentation mistakes can create expensive delays

The administrative side of the federal relief system is strict, and simple paperwork oversights can snowball into serious consequences. Common issues include accidentally leaving creditors off the mailing matrix, providing incomplete income records, or undervaluing household assets on the official schedules. Ask anyone who’s been through a dismissed filing and they’ll tell you: The small details matter more than you’d think.

Filing too late to protect a family vehicle, or transferring real property to a relative right before filing, can also trigger scrutiny from the appointed trustee. Some debtors misunderstand which obligations survive the process, leading to unrealistic expectations about their post-discharge budget and remaining liabilities. With South Carolina courts facing a high volume of cases, judges sometimes have little patience for disorganized or inaccurate petitions.

What Bankruptcy Can and Cannot Do for Your Credit

Yes, bankruptcy hurts your credit at first

To be clear: Filing for bankruptcy is a serious credit event, and it’ll negatively affect your score initially. The exact drop varies depending on your starting point, your existing debt profile, and whether you already have multiple accounts in default. A public record of the filing stays on traditional credit reports for up to ten years, signaling to future lenders that you previously struggled with repayment.

But here’s some perspective. For South Carolinians with debt already in collections, their credit scores may already be taking significant, ongoing damage. The initial drop from bankruptcy is real, but it isn’t necessarily permanent, and for many people, the alternative (years of mounting late fees and collection accounts) is worse.

But many people start rebuilding sooner than they expect

Despite the initial credit hit, a lot of people find that recovery begins sooner than they anticipated. Getting a formal discharge wipes away the legal obligation to pay eligible debts, which can immediately reduce your debt-to-income ratio. Ending past-due accounts and stopping the cycle of late fees may provide a clearer starting point for rebuilding finances, particularly for those facing ongoing financial challenges in a spiral of minimum payments that barely cover interest.

Establishing timely future payments on surviving obligations, using secured credit cards responsibly, and maintaining a realistic budget can steadily improve your standing over time. Eliminating overwhelming unsecured balances may provide local families with an opportunity to improve their financial footing.

Bankruptcy isn’t the right answer for every debt problem

While bankruptcy is a powerful tool, it doesn’t erase every financial obligation. Certain categories of debt usually survive the discharge process, including recent tax liabilities, ongoing child support payments, court-ordered alimony, and most federal student loans. If your primary financial issue is tied to these non-dischargeable obligations, filing a petition may not provide the relief you’re hoping for.

Also, if your setback is temporary and manageable through negotiation, non-bankruptcy alternatives like debt consolidation or creditor workouts may be worth exploring first. It’s worth carefully evaluating whether you need temporary lender forbearance or formal legal relief to protect your vehicle. There’s no one-size-fits-all answer here.

When It Makes Sense to Talk to a Lawyer

Some cases are straightforward, but many aren’t

Some people with minimal assets and simple sources of income choose to represent themselves, and sometimes that works out well. But many cases involve legal variables that can materially change the outcome. Professional review matters most when you own a home, you’re behind on secured debt, or a creditor is actively suing you.

Individuals who’ve recently transferred assets, co-own property with an ex-spouse, or have complex domestic support obligations face heightened risks during the federal review process. Acting without professional guidance can result in permanent loss of property. With South Carolina experiencing some of the nation’s highest foreclosure rates, the timing of legal action often matters just as much as basic eligibility.

The cost of mistakes can be higher than people expect

Trying to navigate federal court without adequate preparation can lead to consequences that far outweigh whatever you saved by going the DIY route. Dismissed cases may remove certain bankruptcy protections, meaning the automatic stay typically ends and creditors may resume collection activity. Debtors who accidentally omit creditors from their schedules may find those debts survive the discharge, leaving them with financial burdens they thought were gone.

Avoidable property exposure, missed filing deadlines, and incorrectly claimed exemptions can all lead to the loss of assets that might otherwise have been protected under state law. Many people wait too long to seek guidance because they assume the process may lead to total financial ruin. It usually doesn’t, but the longer you wait, the fewer options you’ll have.

A Financial Reset Starts with Clear Information

Taking control of a difficult financial situation requires a calm, methodical approach rather than acting out of panic. Bankruptcy is a structured legal tool designed to help honest individuals pursue a fresh start; it isn’t a moral failing or a dead end. Differentiating between Chapter 7 and Chapter 13, recognizing how much timing matters, and gathering the right paperwork can put you in a much stronger position to make smart decisions.

Those facing time-sensitive financial challenges may benefit from seeking guidance as soon as possible. Foreclosure, eviction, and repossession timelines don’t pause on their own. Federal bankruptcy basics from the U.S. Courts website are among the most reliable starting points for understanding your options and keeping the situation from getting worse.

Knowing how South Carolina’s exemptions apply to your personal property can determine whether you keep certain assets during the process. Many families successfully navigate bankruptcy each year, coming out the other side with lower stress, improved cash flow, and a real chance to rebuild their credit. If you’re struggling with overwhelming obligations, educating yourself on these federal protections is the best first step toward recovery you can take.

{kind=link}

{kind=link}